Introducing Modern Treasury Payments. Built to move money across fiat and stablecoins. Learn more →

Why Payment Operations Should Be Part of Your Fintech Stack

Payment operations are central to an efficient, modern fintech stack. Read more about the business challenges and opportunities money movement technology presents.

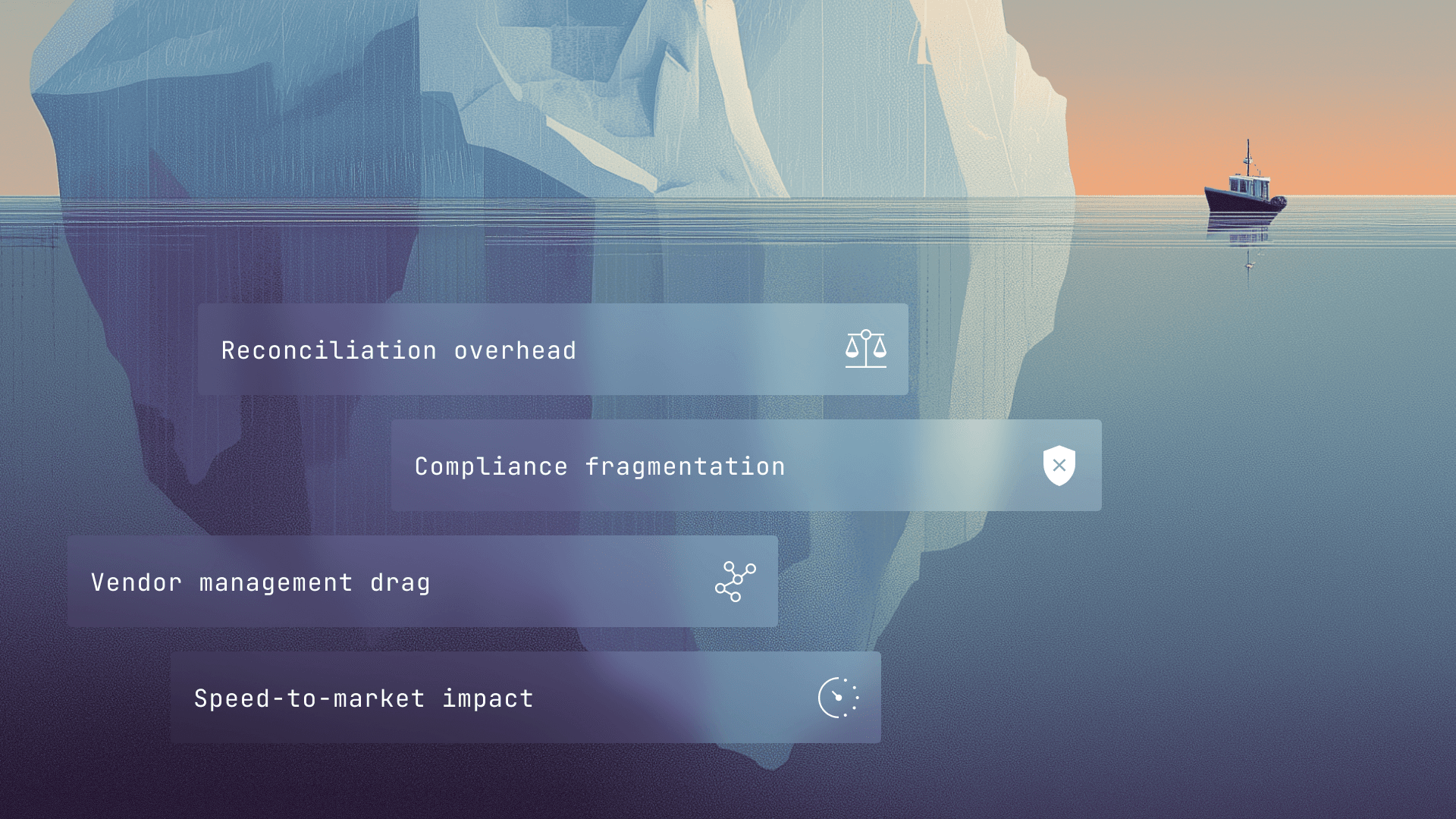

As companies scale, the volume and complexity of financial data and management also scales. Because businesses have options for meeting this demand, growing companies can easily wind up with complicated fintech stacks featuring siloed tools and software. Think: multiple bank accounts, multiple ERPs, legacy systems, discrete finance solutions, and everyone’s favorite, Excel.

Our recent state of payment operations survey revealed that many companies fail to make a comprehensive payment operations platform a part of their tech stack, using an average of 9.5 systems to manage money movement in 2022.

In addition to the resources an overloaded stack can consume, finance professionals with too many tools have a harder time partnering across departments in a meaningful way.

Modern teams (from sales and marketing to engineering and product) increasingly want to leverage company financials to inform and improve their strategy.

And a lack of transparency (with financial data spread across systems) blocks companies from bringing products to market quickly or collaborating efficiently.

In this journal, we’ll explore where payment operations sit in a modern tech stack and why the right solution can help companies streamline workflows and thrive (not just survive) in financial technology’s next chapter. With the growth of embedded payments and big advances in real-time money movement, preparation is key to keeping pace.

Here, Sapphire lays out what they call a “sprawling” fintech stack

Where Do Payment Operations Sit in a Modern Tech Stack?

Payment operations refers to the infrastructure and workflows companies use to move money. These operations include the full lifecycle for every payment, from initiation and funds tracking to reconciliation and ledgering.

In the simplest terms, payment operations sit between your product and your other business systems in a modern tech stack.

Put another way, payment operations facilitate the movement of money: from a product to a bank account, for example, or to multiple bank accounts. When a customer makes a payment to a marketplace or invests through an app, payment operations ensure this money successfully and securely reaches its intended destination.

What may seem simple—moving funds from point A to point B—can be intricate and time-consuming. In fact, according to our recent survey, a strong majority of financial decision makers (69%) think managing payments takes too long from start to finish. This makes sense, given that much of this work is still manual and managed across discrete systems. On average, teams lose 9+ hours per week (over one business day) dealing with payment operations issues (such as delays or failures).

It should be noted that choosing to sit outside the flow of funds often requires additions to your stack, namely reliance on a third-party processor. This route can also prove slower and more costly.

When it comes to growth, the choice to streamline and consolidate technology can have long-reaching positive impacts.

Why Include Payment Operations in Your Stack? 2 Model Innovators

Luckily, it’s possible to streamline payment operations without overhauling your current fintech stack. That said, an end-to-end solution can dramatically cut back on the number of tools (and the amount of toggling) required to move money. Let’s take a look at two reasons the right payments solution matters, as well as model companies taking a modern approach.

1. Successful money movement is vital for scale (Meet Sana)

The infrastructure and workflows required to move money are complex and regularly underestimated. Especially when you consider the full cycle of processes for sending and receiving payments:

- Payment initiation, approvals, and funds tracking

- Payment failure/returns management

- Reconciliation and ledgering

- A robust compliance program.

With tool proliferation, the latter can become even more burdensome. For these reasons, creating a solution in-house (built for scale) can be a big investment.

Consider the team at Sana, a company that provides self-insured health care and employee benefits to small- and medium-sized businesses. Sana processes over $40M in payments across 12 bank accounts and reconciles 1,000+ payments per customer per month.

By the Sana team’s estimates, building a money movement solution in house would cost (at minimum) $70,000 in engineering time to set up, and a further $150,000 in annual engineering and support costs to maintain.

With Modern Treasury’s solution, Sana has completely (and more economically) automated how premiums are funded by employers, with 100% of insurance payments initiated and managed through the platform. Because the solution is scalable and API’s are flexible, Sana can continue to focus on growing to meet their goal: addressing the lack of affordable health care in the United States.

2. Prepare for the future of finance (Meet Parafin)

Money movement is at an inflection point. A challenging market environment raises the stakes for efficient resource allocation (i.e., looming cuts to teams and tech stacks) and customer retention (i.e., mistakes are costly).

Market conditions coupled with accelerating payments technology makes the adoption of modern solutions a business imperative.

Regarding the latter, two major shifts are important to note. First, embedded payments are an expanding (and exciting) opportunity. For companies looking to increase revenue, improve retention, and save money, embedded payments are worth exploring. Projected revenue for these payments is as high as $138 billion in 2026, up from $43 billion in 2021. In fact, by 2030, 73% of global consumer payments will be processed by non-financial institutions.

Second, FedNow will rapidly expand the real-time payments ecosystem in the US—a sizable paradigm shift. Readiness for real-time payments requires both solid banking partnerships and modern payment operations. And some companies, like Parafin, are well ahead of the curve.

As an embedded fintech infrastructure company, well-managed payments and the right tech stack are vital to Parafin’s success. Parafin provides a suite of APIs that abstract the complexity of in-house credit for partners including marketplaces, vertical SaaS tools, and payment processors. Not only was a modern payment operations solution quick (it took 8 hours to implement the Modern Treasury API), it was also financially sound (Modern Treasury helped the team minimize development costs and time to go live). Parafin has also partnered with JP Morgan and Modern Treasury to access RTP rails for instant loan disbursements.

Companies that issue real-time payments have exponentially quicker and more accurate visibility into their finances (and thus, greater control). Customers that receive funds immediately can initiate their own growth and expansion at a faster clip.

Not to mention that end-to-end payment operations tech gives Parafin the tools to manage and report on payment flows to partners, users, and external third-parties. In fact, six different teams at Parafin use Modern Treasury regularly for insight and job execution.

A Fintech Stack Poised for Growth with Modern Treasury

Taking a critical look at your fintech stack, with an eye for efficiency, security, and clarity, is key to business longevity and scalability. If you’re considering a change, and want to learn more, talk to us.

Get the latest articles, guides, and insights delivered to your inbox.

Authors