Introducing Modern Treasury Payments. Built to move money across fiat and stablecoins. Learn more →

What are the Costs of Sitting Inside or Outside the Flow of Funds?

Whether a business chooses to sit in the flow of funds depends on a number of factors. This journal looks at the cost implications of being inside or outside the flow of funds.

We’ve written previously about the different flow of funds models and some of the risks and tradeoffs associated with each. In this journal, we’ll dig deeper into some larger cost implications of being inside or outside of the flow of funds.

Being in the flow of funds means working directly with a bank. The primary costs to consider here are bank fees. Being outside the flow of funds means working with a third-party processor (TPP). The primary costs to consider here are transaction fees charged by them.

Bank Fees

Banks are responsible for the money that moves through accounts at their institution, and in underwriting your business, they accept legal liability associated with moving your money. If your company moves money as part of your business, banks will also be responsible for money that moves through your accounts. As a result, banks may charge higher fees or ask for larger capital reserves to cover any financial risk.

These fees are generally minimal, but they can vary based on a number of factors, including the volume of your transactions, the payment rails you utilize, your business model and your customers, and your bank’s risk tolerance.

If your business receives a chargeback or is unfortunate enough to experience fraud, the fees with your bank may rise because those risk events have weakened your bank’s tolerance for your business. Let’s see how this looks in practice.

Imagine an online marketplace called Eats2Eats that connects buyers and sellers of restaurant equipment. A company called Tasty Sodas logs into Eats2Eats to order a soda machine from the seller, V’s Vending.

The transaction goes from Tasty Sodas through Eats2Eats who will then send money to V’s Vending for the order. But the soda machine is never shipped, and V’s Vending deactivates their account on the Eats2Eats website. Tasty Sodas creates a reversal for their payment, because they never received the item they paid for.

Because they're sitting in the flow of funds for this transaction, Eats2Eats is responsible for repaying Tasty Sodas to make them whole. The bank can also charge them a fee for the reversal of payment (e.g., an ACH Return Code 10).

Processor Fees

The same is true of working with a third-party processor (TPP). Because the TPPs take on the liability of holding the funds while the transaction is processed (and thus have to maintain strict compliance programs), there are typically fees associated with using one. One reason for the high fees is because with multiple customers across many different verticals, and without the knowledge of which businesses are more risky, TPPs need to average the risk of their customers together.

Say Eats2Eats uses a TPP to process ACH payments made through their site. If the previous scenario plays out, Eats2Eats would also owe their TPP a reversal fee, in addition to the fees the TPP already charged on the original transaction as well as bank fees.

This is why, in many instances, it is actually more cost-effective for businesses to sit in the flow of funds, even with the associated risks. By doing so, the business is able to limit certain factors that increase the likelihood of fraud, as well as removing the need for paying a TPP.

For example, Eats2Eats could choose to not release funds until there is confirmation of delivery by Tasty Sodas. Or they may choose to pay out a portion when the deal is done, another when the product is shipped, and another when the product is confirmed to have arrived. There are many ways Eats2Eats can design their payments to mitigate or de-risk their marketplace.

Resources and Maintenance

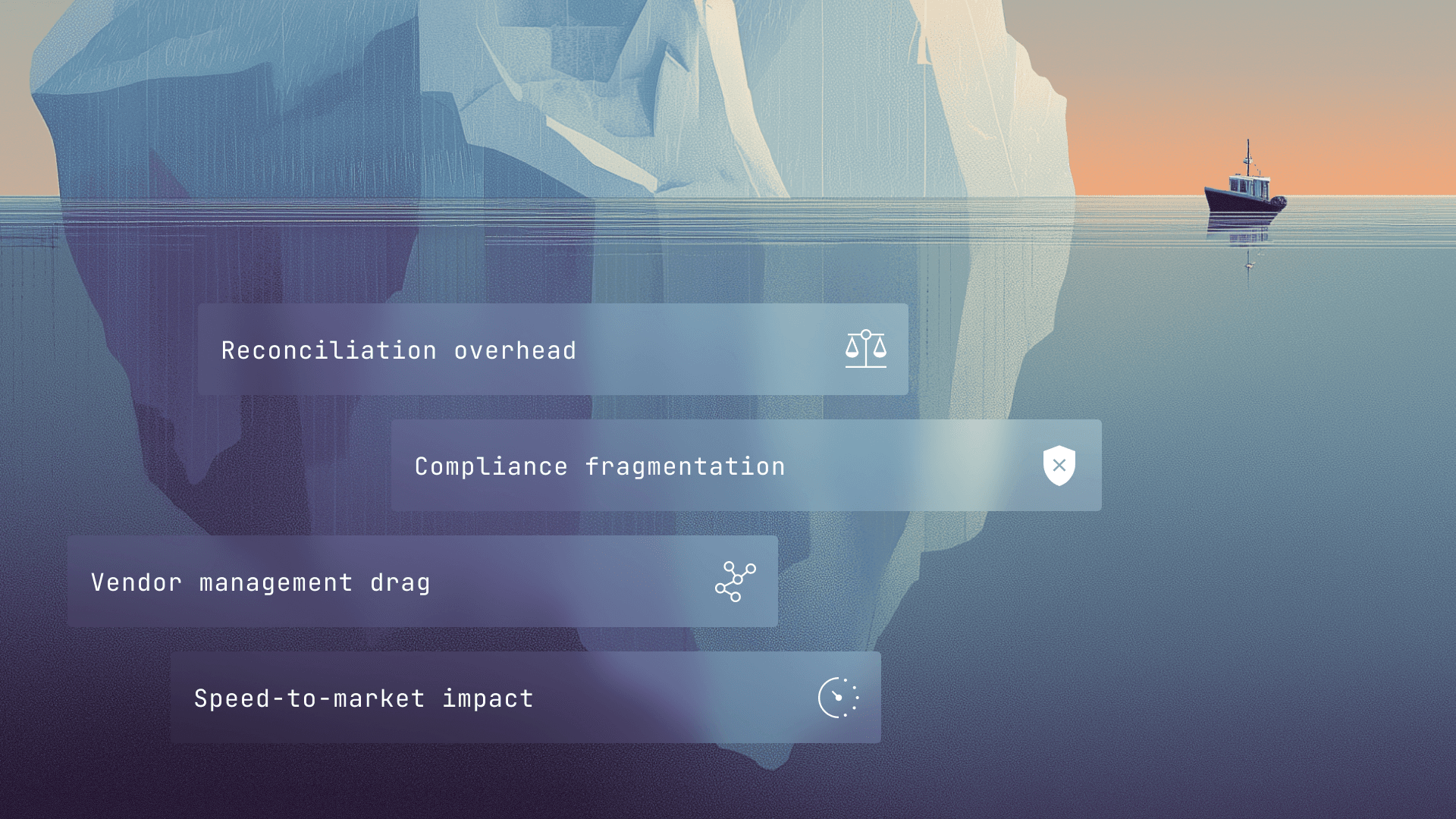

In order for your business to sit in the flow of funds, you need to integrate directly with your bank. When building a custom integration, a company has to take several detailed steps and precautions. This includes working to get to know the bank, managing compliance, learning and following National Automated Clearing House Rules (Nacha) rules, and figuring out how to integrate directly with a bank’s core processing system.

While these steps may not be inherently risky, they can cause ongoing issues for businesses if not done carefully and properly. And not just for payments. Additional workflows—such as automatic reconciliation, managing counterparty information, or adding virtual accounts— can add layers of complexity and compound the risk.

The process of creating, implementing, and maintaining a bank integration as your business grows and changes is also time-consuming, resource-intensive, and ongoing. Businesses that use Modern Treasury are able to bypass the challenging process of building a custom integration and the risks associated with it. We leverage our existing bank partnerships to streamline the bank integration process.

We work with our customers to determine their business-specific needs for payments, to help future-proof their payment operations, and to set up custom controls that can help them mitigate riskier transactions. All of these steps help Modern Treasury customers sit in the flow of funds while lessening the associated risks. And when the risk is lower, so are your costs of doing business.

Next Steps

Deciding whether or not to sit in the flow of funds is a major question to ask when building your business. It can be overwhelming because there are a lot of considerations at play, and much of it is dependent on your business needs.

If you want to talk through your options, get in touch with one of our payments advisors.

Get the latest articles, guides, and insights delivered to your inbox.

Authors

Ryan Jackson is a Senior Product Manager at Modern Treasury. Prior to this role, he served on the Board of Advisors at the Dutch Masters of Scale. He also co-founded and led two companies to successful exits. He holds a B.S. and M.S. in Electrical Engineering and Computer Science from M.I.T.